MAS Monetary Policy Statement - April 2025

INTRODUCTION

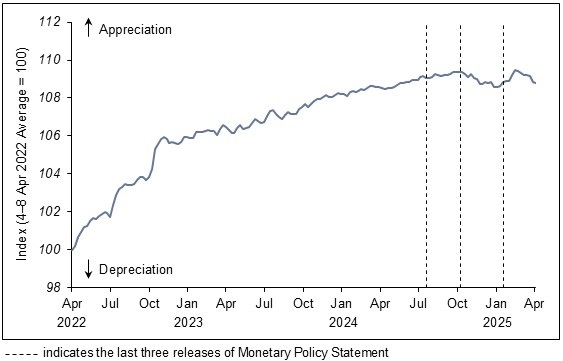

1. In January this year, MAS kept the Singapore dollar nominal effective exchange rate (S$NEER) policy band on a modest and gradual appreciation path, but reduced its slope slightly. There was no change to the width of the policy band or the level at which it was centred. Since then, the S$NEER has fluctuated within the upper half of the policy band in response to shifts in the macroeconomic outlook and shocks to global trade policies. Notwithstanding the volatility, the average level of the S$NEER over the last three months has been broadly unchanged from that in the preceding three months.

Chart 1

S$ Nominal Effective Exchange Rate (S$NEER)

GROWTH BACKDROP

2. Singapore’s key trading partners showed signs of weakening economic activity in the first quarter of 2025. Consumer and business confidence in major economies have fallen alongside escalating trade policy uncertainty. Concomitantly, retail sales and capex intentions have softened. In the region, export performances across economies have turned more uneven, reflecting the waning of temporary boosts to production and shipments from trade frontloading, even as underlying AI-driven demand for electronics saw some resilience.

3. MTI’s Advance Estimates show that the Singapore economy expanded by 3.8% year-on-year in Q1 2025. At the same time, the growth momentum was weaker than expected, contracting by 0.8% on a quarter-on-quarter seasonally-adjusted basis, down from the 0.5% expansion a quarter ago. In tandem with the nascent slowdown in some major economies, activity in the external-facing manufacturing and modern services sectors declined. Meanwhile, the domestic-oriented sectors saw generally tepid activity.

4. Prospects for global trade and GDP growth dimmed in early April. The US has imposed tariffs on imports from most countries in the world, with some of these countries announcing retaliatory tariffs. Economies that levy duties on imports will likely experience an increase in costs and this will weigh on their aggregate demand. At the same time, exporting countries which have been hit by tariffs will be confronted with weaker demand and pressure to lower prices for their output. In addition, global financial conditions have tightened as asset markets have begun repricing risks in the global economy. These factors will exert widespread and potentially reinforcing drags on production, trade, and investments in Singapore’s major trading partners. Global growth is expected to weaken this year, with trade possibly moderating to a greater extent.

5. For 2025 as a whole, Singapore’s GDP growth is expected to slow to 0.0–2.0% from 4.4% last year. Given Singapore’s high trade dependency and deep integration with global supply chains, slowing global and regional trade as well as heightened policy uncertainty will weigh on the external-facing sectors, which could spill over into the domestic-oriented sectors. Consequently, the aggregate level of output will come in below the economy’s potential this year.

6. The external environment remains uncertain. There are downside risks to Singapore’s economic outlook stemming from episodes of financial market volatility and a sharper-than-expected fall in final demand abroad. A more abrupt or persistent weakening in global trade will have significant ramifications on Singapore’s trade-related sectors, and in turn, the broader economy.

INFLATION OUTLOOK

7. MAS Core InflationMAS Core Inflation excludes the costs of accommodation and private transport from CPI-All Items inflation. eased significantly to 0.7% y-o-y in Jan–Feb 2025, from 1.9% in Q4 2024. Inflation fell by more than expected across a wide range of goods and services. Soft consumer spending on F&B services and retail goods domestically, as well as moderating cost pressures, have dampened consumer price increases. Enhanced government subsidies also contributed to lower services inflation. The re-basing of the CPI in January this year accounted for only a small part of the step down in inflation.

8. MAS Core Inflation is now forecast to average 0.5–1.5% in 2025, down from 1.0–2.0% in the January 2025 MPS. The downgrade reflects the lower-than-expected inflation outturns in Jan–Feb as well as an anticipated moderation in the pace of price increases amid the weakening economic outlook. On the external front, imported inflation should be modest, as slowing global demand and lower energy commodity prices dampen imported costs. Domestic unit labour cost increases are also expected to moderate due to easing nominal wage growth and improving labour productivity. Together with softer consumer spending, as well as enhanced government subsidies, these factors should temper inflation in the quarters ahead.

9. CPI-All Items inflation in 2025 is similarly expected to average 0.5–1.5%, down from 1.5–2.5% previously. This reflects in part the low outturns in Jan–Feb as well as the downgrade to the MAS Core Inflation forecast range.

MONETARY POLICY

10. Amid the weakening external outlook, Singapore’s output gap will turn negative. Consequently, imported and domestic cost pressures will remain low and MAS Core Inflation is forecast to stay well below 2%. The risks to inflation are tilted towards the downside.

11. MAS will continue with the policy of a modest and gradual appreciation of the S$NEER policy band. However, the rate of appreciation will be reduced slightly. There will be no change to the width of the band and the level at which it is centred.

12. MAS will closely monitor global and domestic economic developments, and remain vigilant to risks to inflation and growth.

First, please LoginComment After ~